摘 要

債券指數基金經過10余年的發展,已成為我國基金市場特色鮮明的重要組成部分。本文回顧了債券指數基金的發展歷程,總結現階段突出特點,分析了指數編制機構對市場發展發揮的助力作用,并就進一步發展債券指數基金市場提出了建議。

關鍵詞

債券指數基金 債券ETF 中債指數 主題基金

債券指數基金發展歷程

(一)發展伊始

自2011年市場開始出現跟蹤債券指數1的債券指數基金以來,經過10余年的發展,債券指數基金已成為基金市場特色鮮明的重要組成部分。2018年以前,市場處于發展初始階段,指數基金規模較小。據萬得(Wind)數據2,截至2017年末,市場共有35只債券指數基金,總規模204億元,平均產品規模5.8億元,但規模中位數僅為0.59億元。大部分指數基金至今已清算終止,但也留存下來一批經典產品,如2012年成立的首只涵蓋全市場債券的綜合類指數基金,其跟蹤中債-新綜合債券指數,目前仍然是市場上為數不多的綜合類債券指數基金;2016年成立的首批國開行債券指數基金,為后續迅猛發展的政策性金融債(以下簡稱“政金債”)指數基金拉開序幕。

(二)初具規模

2018年債券指數基金發展迅猛,新成立債券指數基金17只。截至2018年末,債券指數基金規模已突破1000億元,是2017年末的5倍。在此基礎上,2019年債券指數基金再次取得突破式發展,年末規模達3600億元,各期限的政金債指數基金大量成立,奠定了以政金債指數基金為主要類型的債券指數基金市場格局。2020年至2023年,債券指數基金的整體規模穩中有升,政金債指數基金仍然占據主導地位,也有部分基金管理人嘗試布局地方政府債、高等級信用債和區域主題債券指數基金。截至2024年3月末,債券指數基金總規模已達6517億元3。

經過近年的發展,目前我國債券指數基金市場已初具規模,但仍處于較為初步的發展階段,其規模占債券型基金的比重不足10%,未來仍有較大的發展空間。

當前我國債券指數基金特點

(一)利率債指數基金為主體,期限分布以短期限為主

債券指數基金包括利率債、信用債及其他類型指數基金,并以利率債指數基金為主體。截至2024年3月末,全市場187只債券指數基金中,有162只為利率債指數基金,規模占比接近90%(其中,政金債指數基金150只,國債指數基金8只,地方政府債指數基金4只);信用債指數基金20只,規模占比 為8%左右;其他類型主要包括綜合類債券指數基金和可轉債指數基金,分別有3只和2只,規模占比較低(見圖1、圖2)。

從期限上來看,債券指數基金以小于3年的短期限4為主。信用債指數基金期限全部集中在短期限。利率債方面,短期限政金債指數基金仍是市場關注的熱點產品,跟蹤中債估值中心、中國外匯交易中心、上海清算所、彭博等指數編制機構發布的短期限政金債指數基金具有相當規模,占比50%以上。2024年上半年,20余只短期限政金債指數基金成立,新成立的基金主要跟蹤0~3年期限指數。

(二)持有人類型以機構為主,但也逐漸成為個人投資者進行資產配置的工具

債券指數基金持有人類型以金融機構為主。根據各基金披露的2023年報,有超過85%的債券指數基金的機構持有比例在90%以上,平均機構持有比例為94%(見圖3)。

雖然債券指數基金主要由機構持有,但也逐漸成為個人投資者進行資產配置的工具。個人投資者直接參與債券市場投資具有一定門檻,而債券指數基金具有透明分散的特征。隨著互聯網平臺等基金代銷渠道帶動產品知名度提升,對于擁有更長歷史業績的產品,個人投資者的參與程度更高。據統計,個人投資者持有比例高于30%且基金規模大于5億元的債券指數基金均在2019年及以前成立。個人投資者主要參與的產品類型包括中長期限利率債和綜合類債券指數基金,債券指數基金相對穩定的收益是吸引個人投資者的主要因素。

(三)創新產品不斷涌現

近年來,基金管理人和債券指數編制機構圍繞債券指數基金進行了諸多創新嘗試,尤其在債券交易型開放式指數基金(ETF)和主題類債券指數基金方面取得了一定的成績,為投資者提供了更為豐富的選擇。

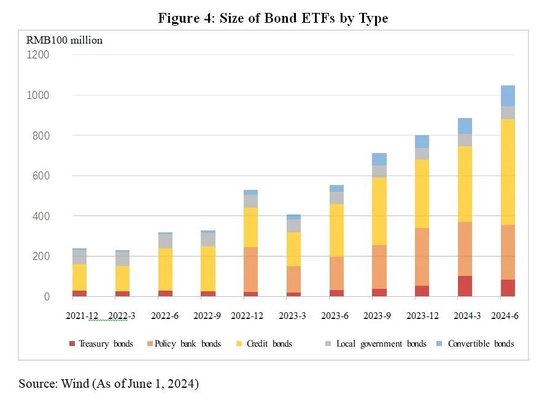

1.債券ETF規模持續上漲

債券ETF作為可以在交易所場內二級市場買賣的債券指數基金,受益于費率優勢和交易便捷,規模不斷上漲。2022年5只政金債ETF成立,規模穩中有升,期限覆蓋0~3年、1~5年、7~10年等各期限,進一步豐富和完善了場內工具型產品種類,為投資者提供了多樣化的利率債投資選擇。在超長期限債券ETF方面,近兩年上市了2只跟蹤30年期國債指數的債券ETF,具備清晰的長久期風險收益特征,有效填補了市場空白,受到投資者的廣泛關注。截至2024年5月末,債券ETF規模突破1000億元,標的債券種類以國債、政金債、信用債、地方政府債、可轉債等為主。

2.主題類產品創新涌現

相較種類豐富的主題類股票指數基金,債券指數基金的主題類產品相對匱乏,產品類型局限在債券品種和債券期限的組合之中。而隨著債券指數編制機構的指數創新,結合投資者的主題投資需求,涌現出一批受到市場認可的創新產品,包括綠色債券指數基金、優選投資級信用債指數基金、綠色普惠主題金融債券指數基金等主題產品。基金管理人布局主題類產品能夠更有針對性地發揮資本市場的價值引導和資源配置作用,為相關領域引入資金支持,更好發揮金融服務高質量發展作用。

中債估值中心助力債券指數化投資

作為國內債券指數基金市場最主要的標的指數編制機構,中債估值中心自2003年開始發布市場首批人民幣債券指數,長期致力于完善中債指數體系、提升指數質量、增強指數研發能力,編制了一系列能夠反映人民幣債券市場、具備表征性和可投資性的指數。伴隨著國內債券指數基金市場的興起和發展,中債指數已成為中國境內歷史悠久、應用廣泛、產品數量眾多的人民幣債券指數品牌,在債券指數化投資的各方面為市場提供專業服務。

(一)做好金融“五篇大文章”,持續豐富指數族系

為響應高質量發展要求,中債估值中心積極拓展金融支持重要領域實體經濟渠道,將科技金融、綠色金融、普惠金融、養老金融、數字金融“五篇大文章”與指數產品編制相結合,為市場投資者提供可落地、可執行的指數化投資解決方案。

一是不斷完善中債綠色及可持續發展系列指數體系,編制發布綠色債券系列指數,滿足綠色債券指數基金跟蹤需求。基于中債環境、社會和公司治理(ESG)評價體系編制發布中債-ESG優選信用債指數,以及10余只與市場機構合作的ESG債券指數。

二是推出科技創新系列債券指數,刻畫科技創新主題債券的回報表現和收益特征,為投資者參與科技創新信用債券投資提供參考和專業化工具。

三是在普惠金融推進全面鄉村振興戰略實施方面,中債估值中心已發布4只鄉村振興主題指數,引導資金流入鄉村振興實施項目,助力農業農村現代化建設。

四是與市場機構聯合發布年金基金債券指數,在養老金指數化投資方面進行開創性探索。

此外,中債估值中心依托債券基礎信息數據積累,針對性識別科技、綠色、普惠、養老、數字相關債券作為指數成分,進一步為債券指數基金和機構定制合作主題類產品提供指數編制服務,推動金融高質量發展。

(二)提供基金份額參考凈值(IOPV)、業績歸因等指數投資衍生服務

為滿足市場對于指數投資衍生服務的需求,中債指數陸續推出IOPV、債券業績歸因、指數業績歸因等數據服務,為債券指數基金和債券ETF的投資決策及業績評價提供參考。

一是上線債券ETF的IOPV計算服務。IOPV作為ETF盤中投資交易的參考指標,對于提高ETF交易透明度和交易活躍度具有重要作用。中債估值中心在2024年4月正式上線債券ETF的IOPV計算服務,首批服務對象為在深圳證券交易所上市交易的華安中債1-5年國開行債券ETF(159649)、博時中債0-3年國開行債券ETF(159650)和平安中債0-3年國開行債券ETF(159651),首次覆蓋政金債ETF,填補了相關市場的空白。

二是推出業績歸因數據服務。為滿足投資者分析投資組合業績來源、衡量投資組合業績表現的需求,中債估值中心于2021年推出中債業績歸因產品,包括單券業績歸因、指數業績歸因和投資組合業績歸因計算工具,投資者可根據持倉進行業績歸因計算,并與指數基準進行比較。業績歸因框架主要基于Campisi模型,將債券收益歸因為持有收益、無風險利率(國債收益率曲線)變動收益、個券風險(信用利差)變動收益三大類共11項因子,為債券指數化投資的收益來源拆解和業績比較評價提供更為豐富翔實的分析數據。

(三)建設中債DQ金融終端指數投研模塊,提供指數化投資便利工具

目前,中債指數已發布超過1500只各類指數,為方便基金管理人和投資者日常應用指數數據和獲取指數信息,中債DQ金融終端圍繞中債指數應用場景持續進行開發優化。

一是在客戶端提供豐富全面的指數基礎指標、統計分析等數據,支持多指數歷史收益風險數據對比分析。

二是從資產類別、熱點主題、樣本期限、信用評級等數十個維度提供指數篩選功能,幫助使用者迅速定位所需要的指數信息。

三是內嵌指數計算器功能,可在線利用中債指數同源數據庫進行自定義規則指數歷史回測,為策略驗證提供支持。

四是可以便捷查詢下載指數衍生服務的深度數據,例如業績歸因、IOPV等相關數據。

進一步推動債券指數基金發展的建議

一是進一步豐富債券指數基金類型。目前債券指數基金品種相對集中在利率債品類,較為缺少綜合類、信用類及主題類產品。參考境外市場,投資者對于投資債券市場的工具型產品需求較大,如貝萊德美國債券綜合指數ETF的規模達1048億美元5,可作為投資者參與整體債券市場投資的一鍵式配置工具,被廣泛使用在投資顧問6的資產配置策略中。建議進一步布局綜合類和信用類債券指數基金,為各類投資者提供豐富便捷的債券市場配置工具。另外,隨著科技、綠色、普惠等主題類債券的不斷發行和豐富,相關債券指數也已陸續發布,主題類產品的進一步發展已具備先決條件,部分金融機構已開始推動主題類債券指數基金的創設與投資。建議進一步加大力度推動主題債券指數基金和債券ETF發展,引導資金投入相關領域,做好金融“五篇大文章”,推動經濟高質量發展。

二是優化債券指數基金投資者結構。作為債券市場的主要參與者,金融機構在債券指數基金的投資參與中具有先天優勢,形成了以銀行類金融機構為主的債券指數基金投資者結構。進一步發展壯大債券指數基金市場離不開更加豐富多元的投資者結構。在金融機構中,養老金、年金和保險資金等中長期資金的投資需求能夠引導產品期限結構均衡發展,改善短期限產品過度集中的情況。境外投資者近年來對于中國債券市場的投資熱度不減,但較少通過債券指數基金進行投資。建議將債券指數基金納入基金互認、ETF互掛、跨境理財通等跨境互聯互通業務,促進境外投資者投資境內債券指數基金。債券指數基金為個人投資者提供了低門檻的債券市場投資參與機會,建議通過基金銷售平臺等渠道宣傳加強個人投資者對于債券市場和債券指數基金的了解,逐步培養投資配置意愿和能力,創設適配個人投資者風險偏好的債券指數基金。

注:

1.2003年成立的長盛全債指數增強基金業績比較基準為債券指數與股票指數的組合,作為債券指數增強基金,本文未將其納入債券指數基金范圍。

2.本文數據除特殊說明,均來源于Wind。

3.本文針對債券指數基金各項統計分析數據均不包含同業存單指數基金。

4.本文短期限為指數平均久期小于3年,中期限為指數平均久期3~5年,長期限為指數平均久期5~10年,超長期限為指數平均久期10年以上。

5.數據來源:BlackRock,截至2024年3月31日。

6.該產品70%的投資者為投資顧問。投資顧問公司主要提供投資建議和管理服務,類似國內的證券公司投資顧問部門、私人銀行部門、專業第三方理財咨詢公司。根據美國投資顧問協會(Investment Adviser Association)2023年報告,投資顧問行業管理規模達到114.1萬億美元,全美有15114家注冊投資顧問公司,全行業90.6%的資產集中于管理規模在50億美元以上的大公司。

參考文獻

[1] 陳子越,曹陽.中國債券指數基金發展回顧及前景展望[J].中國貨幣市場,2023(4).

[2] 厲海強.中外債券指數基金產品對比及啟示[J]. 債券,2020(10).DOI: 10.3969/j.issn.2095-3585.2020.10.017.

[3] 廖倩蕓,盛曉虹,孫若陽.指數化投資:中國債券市場投資新視角[J]. 債券,2020(11).DOI: 10.3969/j.issn.2095-3585.2020.11.016.

◇ 本文原載《債券》2024年7月刊

◇ 作者:中債金融估值中心有限公司指數部 葛量

◇ 編輯:廖雯雯

Analysis of China Bond Index Fund Market Development

Ge Liang

Abstract

After development for more than a decade, the bond index funds have become an important and distinctive part of China’s fund market. This paper reviews the history of bond index funds, summarizes their prominent characteristics in the current stage, analyzes the index providers’ role in driving market development and gives suggestions on advancing the bond index fund market.

Keywords

Bond index funds, bond ETF, ChinaBond indexes, thematic funds

History of Bond Index Funds

i. Beginning

Since the first bond index fund tracking a bond index1 emerged in 2011, the bond index funds have become an important and distinctive part of China’s fund market. The market was in its infancy before 2018 with a small size of index funds. According to Wind data2, there were 35 bond index funds in the market as at the end of 2017 with a total scale of RMB20.4 billion, averaging RMB580 million per product, in sharp contrast to a median of merely RMB59 million. Most of these index funds have been liquidated and terminated so far, but a number of classic products are still in existence. For example, the first composite index fund covering all bonds in the market, established in 2012 to track the ChinaBond New Composite Index, remains one of the few general bond index funds available in the market now. The first group of CDB bond index funds created in 2016 ushered in a boom of the policy bank bond index funds.

ii. Thriving

Bond index funds thrived in 2018, with 17 products created in the year alone. As at the end of 2018, bond index funds broke the mark of RMB100 billion, five times that in 2017. The year 2019 saw bond index funds make leapfrog moves and hit a size of RMB360 billion at the end of the year, with policy bank bond funds of various tenors established to shape a market landscape dominated by policy bank bonds. The size of bond index funds expanded steadily from 2020 to 2023, while policy bank bonds still dominated the market. Some fund managers tried making a foray into local government bonds, high-grade credit bonds and regional themed bond index funds. As at the end of March 2024, the total scale of bond index funds reached RMB651.7 billion3.

China’s bond index fund market has had a fairly large scale now after its rapid development in recent years, yet still in the early stage. Accounting for less than 10% of the bond fund market, bond index funds still see vast space of growth.

Characteristics of China’s Bond Index Funds at Present

i. Interest rate bond index funds and short terms are the majority

The bond index funds include interest rate bond index funds, credit bond index funds and others, among which the interest rate bond index funds take the lion’s share. As of the end of March 2024, 162 of the 187 bond index funds in the market are interest rate bond index funds (including 150 policy bank bond index funds, 8 treasury bond index funds, and 4 local government bond index funds), accounting for nearly 90% of the total. There were 20 credit index funds, accounting for about 8%. Others were 3 composite bond index funds and 2 convertible bond index funds, representing a fairly low proportion (see Figure 1 and Figure 2).

By terms, bond index funds are mainly short-term4 (less than 3 years). In particular, all credit bond index funds fall in the category of short terms. In terms of interest rate bonds, short-term policy bank bond index funds remain the focus of market participants. The short-term policy bank bond index funds tracking the bond indexes published by ChinaBond Pricing Center, China Foreign Exchange Trade System, Shanghai Clearing House and Bloomberg have reached quite a large scale, accounting for over 50% of the total. In the first half of 2024, more than 20 short-term policy bank bond index funds were established, which mainly track 0-year to 3-year indexes.

ii. Bond index funds are held mainly by institutional investors, with a growing share held by individual investors

The holders of bond index funds are mainly financial institutions. According to the 2023 annual reports disclosed by funds, over 85% of bond index funds were over 90% held by institutions, with the institutional holdings averaging 94% (see Figure 3).

Bond index funds, though held mainly by financial institutions, are gradually becoming a component of individual investors’ portfolio. Individual investors have to meet certain threshold to directly participate in the bond market, while bond index funds are transparent and decentralized. As online platforms and other distribution channels boost the visibility of fund products, the products with a longer track record see greater participation by individual investors. According to statistics, all the bond index funds with a size of over RMB500 million and more than 30% held by individual investors were established in 2019 or before. Individual investors mainly participate in medium-/long-term interest rate bond funds and composite bond index funds. The relatively stable return on bond index funds is the major appeal to individual investors.

iii. Innovative products are mushrooming

In recent years, fund managers and bond index providers have made many innovative attempts on bond index funds. In particular, they have made achievements in bond ETFs and thematic bond index funds.

1. Bond ETFs have been expanding in size

Bond ETFs as bond index funds traded on the secondary exchange market have seen their scale expanding on lower fee rates and convenient trading. Five policy bank bond ETFs were created in 2022, with the size increasing steadily and the terms covering 0-3 years, 1-5 years and 7-10 years. These products have further added to exchange-traded instruments, providing investors with a variety of interest rate bond funds. In terms of ultra-long-term bond ETFs, two ETFs tracking 30-year treasury bonds were launched in the past few years, showing clear risk-return characteristics of long duration, filling the market gap and drawing wide attention among investors. As of the end of May 2024, bond ETFs exceeded RMB100 billion in size, with the underlying bonds mainly being treasury bonds, policy bank bonds, credit bonds, local government bonds and convertible bonds.

2. Innovative thematic products have surged

Compared with the wide variety of thematic equity index funds, the thematic bond index funds are relatively limited, with the product category simply being a combination of bond type and bond term. However, a large number of innovative products recognized by market participants have emerged amid the index innovations by bond index providers and investors’ demand for thematic investment. These innovative products include green bond index funds, selected investment-grade credit bond index funds and green and inclusive financial bond index funds. With an exposure to thematic products, fund managers will give better play to the role of capital markets in guiding value and allocating resources, channeling capital into relevant sectors and better serve high-quality development.

ChinaBond Pricing Center Has Given a Boost to Bond Index-based Investment

As the major index provider in China’s bond index fund market, ChinaBond Pricing Center issued the first batch of RMB bond indexes in 2003. The center has been long dedicated to improving the ChinaBond index series, improving the quality of indexes and enhancing its index research and development capability. It has compiled a series of indexes with representativeness and investability that mirror the RMB bond market. With the domestic bond index fund market emerging and growing, ChinaBond indexes have become a RMB bond index brand featuring a long history, extensive application and numerous products, providing professional services for the market in every respect of bond index-based investment.

i. Continuing to expand the index families with a focus on Five Priorities

To meet the requirements of high-quality development, ChinaBond Pricing Center has expanded the channels of financial support for important sectors of the real economy, and aligned the compilation of indexes with the Five Priorities, that is, technology finance, green finance, inclusive finance, pension finance and digital finance, providing investors with viable index investment solutions.

First, ongoing improvements have been made to the ChinaBond Green and Sustainability Index series, with green bond indexes compiled and published to meet the tracking needs of green bond index funds. The center compiled and issued the ChinaBond ESG Select Credit Bond Index and over ten ESG bond indexes in cooperation with market entities.

Second, the technological innovation bond index series was launched to reflect the return and yield performance of technological innovation-themed bonds, providing a reference and professional tool for investors to invest in technological innovation credit bonds.

Third, in terms of inclusive finance driving implementation of the rural revitalization strategy, ChinaBond Pricing Center has issued four rural revitalization indexes guiding capital flows into rural revitalization projects, thereby contributing to the agricultural and rural modernization.

Fourth, annuity fund bond indexes were launched jointly with market entities, representing groundbreaking explorations in pension index-based investment.

ChinaBond Pricing Center has identified technological, green, inclusive, pension and digital bonds as index constituents based on its basic bond data accumulation, and provided index services for cooperative thematic products customized for bond index funds and institutions, giving an impetus to high-quality development of financial services.

ii. Providing index investment derivative services such as indicative optimized portfolio value (IOPV) and performance attribution

To meet the market demand for index investment derivative services, ChinaBond Indexes have launched IOPV, bond performance attribution, index performance attribution and other data services to provide reference for investment decision making and performance evaluation relating to bond index funds and bond ETFs.

First, the IOPV calculation service for bond ETFs has been launched. As a measure of an ETF’s intraday value, IOPV plays an important role in improving the transparency and activity of ETF transactions. ChinaBond Pricing Center officially launched the IOPV calculation service of bond ETFs in April 2024. The first group of served ETFs are HuaAn ChinaBond 1-5 Year CDB Bond ETF (159649), Bosera ChinaBond 0-3 year CDB Bond ETF (159650) and Ping An ChinaBond 0-3 year CDB Bond ETF (159651) listed on the Shenzhen Stock Exchange, covering for the first time the policy bank bonds ETFs and filling the gap in the related market.

Second, the performance attribution data service was launched. In order to meet investors’ needs to analyze the source of portfolio performance and measure the performance of portfolios, ChinaBond Pricing Center launched ChinaBond performance attribution products in 2021, including calculation tools for bond performance attribution, index performance attribution and portfolio performance attribution, allowing investors to calculate performance attribution based on their holdings and compare them with the index benchmark. The performance attribution framework is mainly based on the Campisi model, attributing bond returns to 11 factors in three categories: holding period return, return on risk-free interest rate (treasury yield curve) change, and return on bond risk (credit spread) change, providing more thorough and detailed analysis data for the yield breakdown and performance comparison of bond index-based investment.

iii. Developing the ChinaBond DQ financial terminal index investment and research module to provide index-based investment facilitation tools

At present, over 1,500 ChinaBond indexes have been released. In order to facilitate fund managers and investors in day-to-day access to and use of index data, the ChinaBond DQ financial terminal continues with development and optimization relating to the application scenarios of ChinaBond indexes.

First, a full range of basic index indicators and statistical analysis data are provided on the ChinaBond DQ to support the comparative analysis of multi-index historical return and risk data.

Second, an index screening function is provided under dozens of dimensions, including asset class, hot topics, terms of constituents and credit rating, helping users quickly locate the index information they need.

Third, the index calculator function is embedded to enable index backtesting under customized rules using the ChinaBond index homologous database online, providing support for strategy verification.

Fourth, the in-depth data on index derivative services are available for inquiry and downloading, such as performance attribution and IOPV data.

Suggestions on Promoting Development of the Bond Index Funds

First, more types of bond index funds should be introduced. At present, bond index funds are concentrated in the interest rate bond category, showing a lack of composite, credit and thematic categories. As seen in overseas markets, investors have a huge demand for instruments designed to invest in the bond market. For example, the size of the BlackRock iShare Core U.S. Aggregate Bond ETF has reached USD104.8 billion5, which can serve as a one-click allocation tool for investors to participate in the bond market and is widely used in the asset allocation strategies of investment advisors6. It is suggested to develop composite and credit bond index funds to provide investors with a wide range of convenient tools for bond allocations. In addition, with a growing variety of thematic funds including technological, green, and inclusive bonds issued, relevant bond indexes have also been released one after another. Seeing thematic products ready for further development, some financial institutions have begun their push for creation and investment of thematic bond index funds. It is suggested to strengthen efforts to develop thematic bond index funds and bond ETFs, channel funds into related sectors and fuel high-quality economic development with a focus on the Five Priorities.

Second, the investor base for bond index funds should be optimized. As main participants in the bond market, financial institutions have inherent advantages in bond index fund investment. A bond index fund investor base dominated by banking institutions has taken shape. Further growth of the bond index fund market cannot go without a more diverse investor base. Among financial institutions, the investment demand from medium- and long-term funds such as pensions, annuities and insurance funds will help balance the mix of product terms and ease the over-concentration in short-term products. Overseas investors have always had a keen interest in investing in China’s bond market in recent years, yet less through bond index funds. It is suggested that bond index funds be included in cross-border connectivity services such as mutual recognition of funds, cross-listing of ETFs and Cross-boundary Wealth Management Connect, so as to boost overseas investments in domestic bond index funds. Bond index funds lower individual investors’ threshold to access the bond market. It is suggested to enhance individual investors’ understanding of the bond market and bond index funds through fund distribution platforms and other channels, gradually foster their willingness and ability to invest, and create bond index funds tailored to individual investors’ risk appetite.

This article was first published on Bond Monthly ( Jul. 2024).Please indicate the source clearly when citing this article. The English version is for reference only, and the original Chinese version shall prevail in case of any inconsistency.

Notes:

1.The performance benchmark of Changsheng All Bond Index Enhanced Bond Fund, established in 2003, is a combination of bond and equity indexes. As a bond index enhanced fund, it is not included in the bond index funds in this paper.

2.Unless otherwise specified, all data in this paper are from Wind.

3.All statistical analysis data on bond index funds in this paper exclude inter-bank certificate of deposit index funds.

4.In this paper, short terms mean an average index duration of less than 3 years, medium terms mean an average index duration of 3 to 5 years, long terms mean an average index duration of 5 to 10 years, and ultra-long terms refer to an average index duration of more than 10 years.

5.Source: BlackRock, as of March 31, 2024.

6.70% of the investors in this product are investment advisers. Investment advisory companies mainly provide investment advice and management services, similar to the investment advisory departments of securities companies, private banking departments, and professional third-party financial consulting firms in China. According to the 2023 report of the Investment Adviser Association of the United States, the investment adviser industry has reached USD114.1 trillion in assets under management (AUM), there are 15,114 registered investment advisory companies in the United States, and 90.6% of the assets in the industry are concentrated in large companies with more than USD5 billion in AUM.

References

[1] Chen Ziyue, Cao Yang. Review and Outlook on Bond Index Funds in China [J]. China Money, 2023(4).

[2] Li Haiqiang. Chinese and Foreign Bond Index Fund Products: Comparison and Aspirations [J]. China Bond, 2020(10).DOI: 10.3969/j.issn.2095-3585.2020.10.017.

[3] Liao Qianyun, Sheng Xiaohong, Sun Ruoyang. Indexed Investment: A New Perspective on Investment in Chinese Bond Market [J]. China Bond, 2020(11).DOI: 10.3969/j.issn.2095-3585.2020.11.016.

◇ Author from: Index Department, ChinaBond Pricing Center Co., Ltd.

◇ Editor: Liao Wenwen

責任編輯:趙思遠

VIP課程推薦

APP專享直播

熱門推薦

收起

24小時滾動播報最新的財經資訊和視頻,更多粉絲福利掃描二維碼關注(sinafinance)